Protection Designed for the People Who Matter Most

Clarity, transparency, and expert guidance for your family’s financial future.

Strategy Before the Policy

Transparent, expert guidance for life insurance and annuities. We don’t just find you a plan; we build your family’s financial foundation.

“No-obligation consulting. Independent expertise.”

Three Pillars of Protection

Modern Life Insurance & Living Benefits

Protection for life, not just the end of it

Most people think life insurance only pays out at the end. We specialize in policies with Living Benefits—allowing you to access your death benefit early if you face a chronic, critical, or terminal illness. Whether it’s a Term, Whole Life, or a Indexed Universal Life (IUL) policy, we ensure your coverage provides a financial lifeline when you need it most.

Wealth Accumulation & Annuities

Growth you can depend on

Security is about more than just a safety net; it’s about building a foundation. We design Annuity and Cash Value strategies that turn your savings into a guaranteed stream of income. By focusing on tax-advantaged growth and market-resilient structures, we help you transition from the accumulation phase to a worry-free retirement.

The Legacy Audit & Carrier Strength

Traceable decisions and institutional stability

A policy is only as strong as the company backing it. We provide comprehensive Policy Audits that go beyond the surface. We evaluate your current coverage against your 2026 goals, review the Financial Strength Ratings of your carriers (AM Best, S&P), and ensure your beneficiaries are correctly aligned with your estate plan.

Why Living Benefits?

In 2026, life insurance is a tool for the living. It’s about having the choice to use your benefits to cover medical costs or replace income during a health crisis, keeping your family’s lifestyle intact.

FAQs

The Foundation of Coverage

What are “Living Benefits,” and how do they work?

Living Benefits allow you to access a portion of your life insurance policy’s death benefit while you are still alive if you are diagnosed with a qualifying chronic, critical, or terminal illness. Essentially, it transforms your policy from a “death benefit” into a “life-support fund” to help cover medical bills or replace lost income during a health crisis.

Why should I care about a Life Insurance Company’s “Financial Strength Rating”?

A life insurance policy is a long-term promise that may not be called upon for decades. Ratings from agencies like AM Best or S&P tell you if the company has the financial stability to keep that promise. At Nepalee Business Ventures, we prioritize carriers with “A” or better ratings to ensure your legacy is backed by a rock-solid institution.

I already have a policy; why do I need a “Legacy Audit”?

Life moves fast. A policy that worked for you five years ago might be outdated today due to income changes, a new home, or the birth of a child. An audit ensures your coverage amounts, beneficiary designations, and carrier stability still align with your current 2026 reality.

I have life insurance through my employer. Why would I need a separate policy?

In the modern workforce, portability is the ultimate security. Relying solely on “Group Life” through an employer is one of the most common risks families take. Here is why a private policy is essential:

Portability: If you leave your job, your coverage usually ends. A private policy stays with you regardless of your career path.

Control: Employer plans are “one size fits most.” A private policy is customized to your specific debt, income, and legacy goals.

Cost & Health: As you get older, private insurance becomes more expensive. Locking in a private policy while you are young and healthy ensures you are protected even if you develop health issues that make you “uninsurable” later.

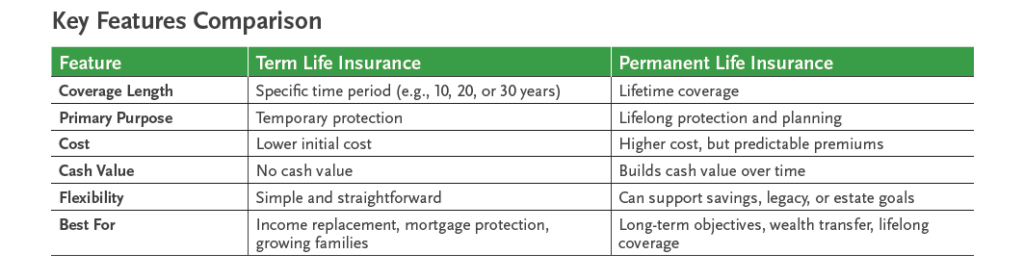

Term vs. Permanent Insurance: Which one do I actually need?

Term Insurance

Term Insurance is like renting; it provides high coverage for a specific period (10, 20, or 30 years) at a lower cost. It’s perfect for protecting “temporary” needs like a mortgage or until children are grown.

Permanent Insurance

Permanent Insurance (Whole Life, VUL, IUL) is like owning; it’s designed to last your entire life, and it builds cash value over time. The Nepalee Approach: Most families benefit from a “laddered” approach—using a mix of both to ensure they have high protection now and a lasting legacy later.

Comparison Chart

What is an Indexed Universal Life (IUL) policy?

An IUL is a type of permanent life insurance that allows the cash value to grow based on the performance of a market index (like the S&P 500). It offers a “floor”, meaning your cash value won’t lose money due to market downturns, but it also has a “cap” on the maximum gains

Building a Foundation for the Next Generation

Should I purchase life insurance on my child?

While no one wants to think about the unthinkable, a policy for a child is primarily about guaranteeing their future insurability and their financial future. By locking in a policy now, you ensure they have coverage regardless of any health issues they may develop later in life. Additionally, many permanent policies for children build cash value that can be accessed later for major life milestones, like a college tuition supplement or a down payment on their first home. Most insurance policies today also offer optional riders that will allow the child to increase their insurance coverage when they reach certain milestones in life.

At what age can I start a policy for my child?

In most cases, you can apply for a policy for a child as early as 14 days old. Starting early allows for the lowest possible premiums and the maximum time for the policy’s cash value to benefit from compound growth.

Am I too young to buy an annuity?

You are never too young to plan for your future and an annuity may be a good choice for your long-term savings goals, such as for retirement. The question you need to ask yourself is – “will I need to access the money before I am 59 ½?” Although you can take a distribution from an annuity prior to age 59 ½, the distribution may be subject to a 10% premature distribution penalty. If you think you may need to access this money on a more short term basis, an annuity may not be the right savings vehicle for you.

What happens if I can’t make my life insurance premium payment?

If your insurance protection is Term life, you will have a grace period to make your payment. If by the end of the grace period you have not made a payment, your policy will lapse and you will no longer have coverage.

If your insurance protection is permanent life insurance, you will have a grace period to pay your premium plus some additional options. It may be possible that your policy has sufficient cash value to pay the premium from those policy values. Just be aware that using policy values and benefits to pay the premium due will reduce the policy’s cash value and death benefit, and may increase the risk of lapsing the policy. If you don’t have sufficient cash value to pay the policy premiums, you may have the option to reduce your face amount to a level that doesn’t require a premium payment.

“No-obligation consulting. Independent expertise.”

Why Choose Us?

Transparent Foundations: “We don’t believe in jargon. We believe in traceable decisions—ensuring you understand every clause and every cost.”

Vertical Flexibility: “Our strategies are built to grow with you, whether you’re starting a family, launching a business, or planning your estate.”

Legacy-Focused: “We look beyond the numbers. We see the family, the business, and the legacy behind the policy.”

A life insurance policy is not ‘set it and forget it’ technology. It is a financial instrument that must be tuned to the rhythm of your life. If you checked ‘No’ on any of these, or if you found yourself confused by your own policy documents, you are exactly the person I built this practice for.